| Key Takeaways

· PMMY has evolved into a powerful instrument of empowerment and aspiration, with 57 crore+ loans amounting to ₹40.07 lakh crore. · Easy credit access with four distinct loan categories: Shishu, Kishor, Tarun and TarunPlus. · Collateral-free loans up to ₹20 lakh for activities covering manufacturing, trading, services & allied agricultural activities. · Strengthening financial inclusion with about 60% of loan accounts belonging to women and about 21% to new entrepreneurs in FY 2024-25. · Over the past decade, PMMY has progressed into a more technology-driven, integrated and sustainable lending framework. |

NEW DELHI, APRIL 08, 2026: Across India’s cities, towns and villages, millions of small entrepreneurs sustain local economies through modest yet vital enterprises, ranging from neighbourhood shops and repair services to small-scale manufacturing and transport activities. These micro businesses not only generate livelihoods but also support employment and essential services at the community level. However, for years, their growth was constrained by limited access to bank credit. Many relied on borrowing from friends, family, or local moneylenders, as they often lacked collateral and formal financial records required by institutions.

The launch of the Pradhan Mantri MUDRA Yojana (PMMY) on 8 April 2015 marked a decisive step in bridging this gap. With the vision of “Funding the Unfunded,” the scheme improves credit access and offers collateral-free loans up to ₹20 lakh. Borrowers include non-corporate, non-farm micro and small enterprises across manufacturing, trading, services, and allied agricultural activities.

Notably, as of 27th March 2026, the scheme has disbursed loans worth ₹40.07 lakh crore with over 57 crore accounts. Besides, 12 crore+ accounts belong to new entrepreneurs– highlighting PMMY’s role in bringing them into the formal financial system.

Over the past decade, PMMY has evolved into a powerful instrument of empowerment and aspiration. In doing so, it has strengthened grassroots entrepreneurship, deepened financial inclusion, and supported sustained growth of India’s local economies.

| Driving Credit to the Last Mile: The Architecture |

PMMY operates through a three-tier institutional structure comprising the Micro Units Development and Refinance Agency Ltd. (MUDRA), Member Lending Institutions (MLIs), and Beneficiaries (borrowers). This framework enables seamless flow of credit from formal financial institutions to micro enterprises through an intermediary-driven model.

| DID YOU KNOW?

In FY 2024-2025, MUDRA Ltd. reported its highest-ever profit of over ₹827 crore, strengthening its journey towards self-sustainability while continuing to support its intermediary partners. |

The Micro Units Development and Refinance Agency, serves as the supporting institution that provides refinance support to a network of lending institutions, enabling the flow of institutional credit to the micro enterprise sector. Loans under PMMY are extended through MLIs, including Scheduled Commercial Banks (SCBs), Regional Rural Banks (RRBs), Small Finance Banks (SFBs), Non-Banking Financial Companies (NBFCs), and Micro Finance Institutions (MFIs). These institutions are responsible for direct lending to the borrowers, ensuring last-mile delivery of credit.

The borrowers under PMMY comprise micro enterprises engaged in manufacturing, trading, services, and allied agricultural activities. They access collateral-free loans to support income generation activities, sustain business operations, and expand their enterprises. Through a structured framework, PMMY facilitates inclusive access to finance and promotes entrepreneurship.

PMMY Coverage

Mudra loans are extended for a wide range of activities that promote income generation and employment creation. These loans are primarily provided for:

- Business loan for vendors, traders, shopkeepers and other service sector activities, such as community, social & personal services, food products, textiles etc.

- Working capital loans through MUDRA cards

- Equipment finance for micro units such as purchase of necessary machinery, equipment etc.

- Transport vehicle loans for commercial use only such as auto rickshaws, small goods transport vehicles, 3 wheelers, e-rickshaws etc.

- Loans for agri-allied non-farm income generating activities such as pisciculture, bee keeping, poultry, livestock-rearing, grading, sorting, aggregation agro-industries, dairy, fishery, agri-clinics and agri-business centres, food & agro-processing, etc.

| Supporting Enterprises at Every Stage with Distinct Loans |

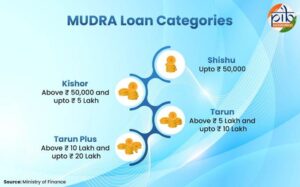

In order to enable easy credit access based on the business requirements, loans under PMMY are classified into four distinct categories namely; Shishu, Kishor, Tarun and Tarun Plus. The categorization caters to different stages of growth and financial needs of the enterprises.

Shishu

The Shishu category covers loans up to ₹50,000 and is intended for very small or early-stage business activities. It typically supports individuals who are starting new enterprises or operating at a minimal scale, including activities such as small retail outlets, repair services etc. The accessibility of the Shishu category loan includes entrepreneurs with no credit history or collateral. This provision helps even the most marginalised entrepreneurs to transform an idea into an actual business.

Kishor

The Kishor category includes loans above ₹50,000 and up to ₹5 lakh. This category is designed for new as well as enterprises that have already commenced operations and require additional funds for stabilisation, working capital or modest expansion of business activities.

Tarun

The Tarun category covers loans above ₹5 lakh and up to ₹10 lakh. It supports growing enterprises seeking to scale up operations, invest in equipment or increase production capacity.

Tarun Plus

The newest category of PMMY- Tarun Plus category, started in 2024, extends loans above ₹10 lakh and up to ₹20 lakh to borrowers who have successfully repaid previous loans under the Tarun category and demonstrated a stable business track record. The provision enables further expansion and progression to higher levels of enterprise activity.

| PMMY: A Catalyst for Inclusive Growth & Development |

PMMY has achieved significant success in the recent times. It has not only deepened financial inclusion but also strengthened entrepreneurship leading to inclusive growth and development. The performance in FY 2024-25 reflects that the core focus of PMMY has been on credit access, women-led enterprises, and formalising micro businesses to create a lasting socio-economic impact.

- Among all states, Uttar Pradeshrecorded the highest loan disbursement at ₹58,111 crore, followed by Bihar with ₹54,064 crore, while Maharashtra ranked third at ₹50,762 crore.

- Women borrowersaccounted for 59.81% of the total number of loan accounts, with total share of 37.45% in disbursed amount.

- New entrepreneursconstituted 21% of total loan accounts and accounted for a 30.09% share of the total disbursed amount.

- The cumulative share of SC, ST, and OBC categoriesstood at 45.52% in terms of loan accounts and 31.77% in terms of the total disbursed amount.

In doing so, the scheme continues to play a vital role in democratizing finance and supporting the growth of micro-enterprises across India.